Design

Thoughts on CRED's design

10 August 2024

CRED is a $6.4 billion startup. But does it deserve such a rich valuation? After all, it's just a credit card reminder app. For starters, CRED does more than reminding you to pay your credit card bills on time. The idea of catering to the top 1% financially credible Indians seems more than a marketing trope to me.

Most Indians are short on cash. Securing bank loans is extremely arduous, embarrassing and seems not worth the effort. With all the data CRED has, it's only sensible that they provide quick credit to "credible" people and earn from interest on the side. That is what they have been doing — their loan book is up to ₹10,000 crore now. In a society where people like to flaunt their status, quick credit definitely helps.

If your product is meant for a premium throng though, the design needs to convey that. And unsurprisingly, since most bank apps allow you to pay CC bills on time, it becomes vital. In fact, you have more control on your card when you use the bank app. Why do people use CRED then? For me at least, it was the "supposed" ease of use in managing multiple cards from a single app.

And since the animations are so fun, I use CRED as my primary UPI app too! I also like the fact that playing silly games earn me a couple hundred rupees off on my next CC bill.

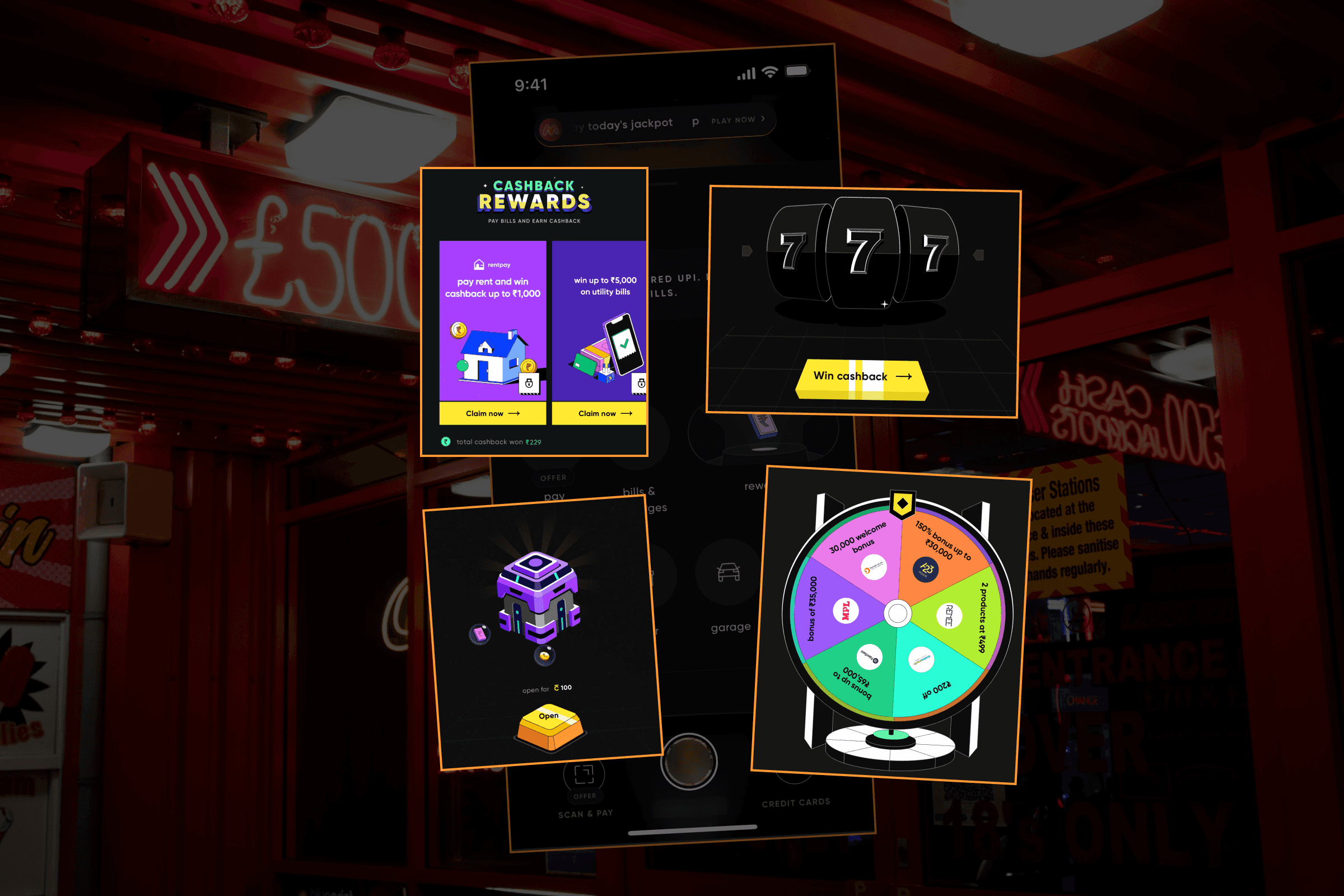

The design

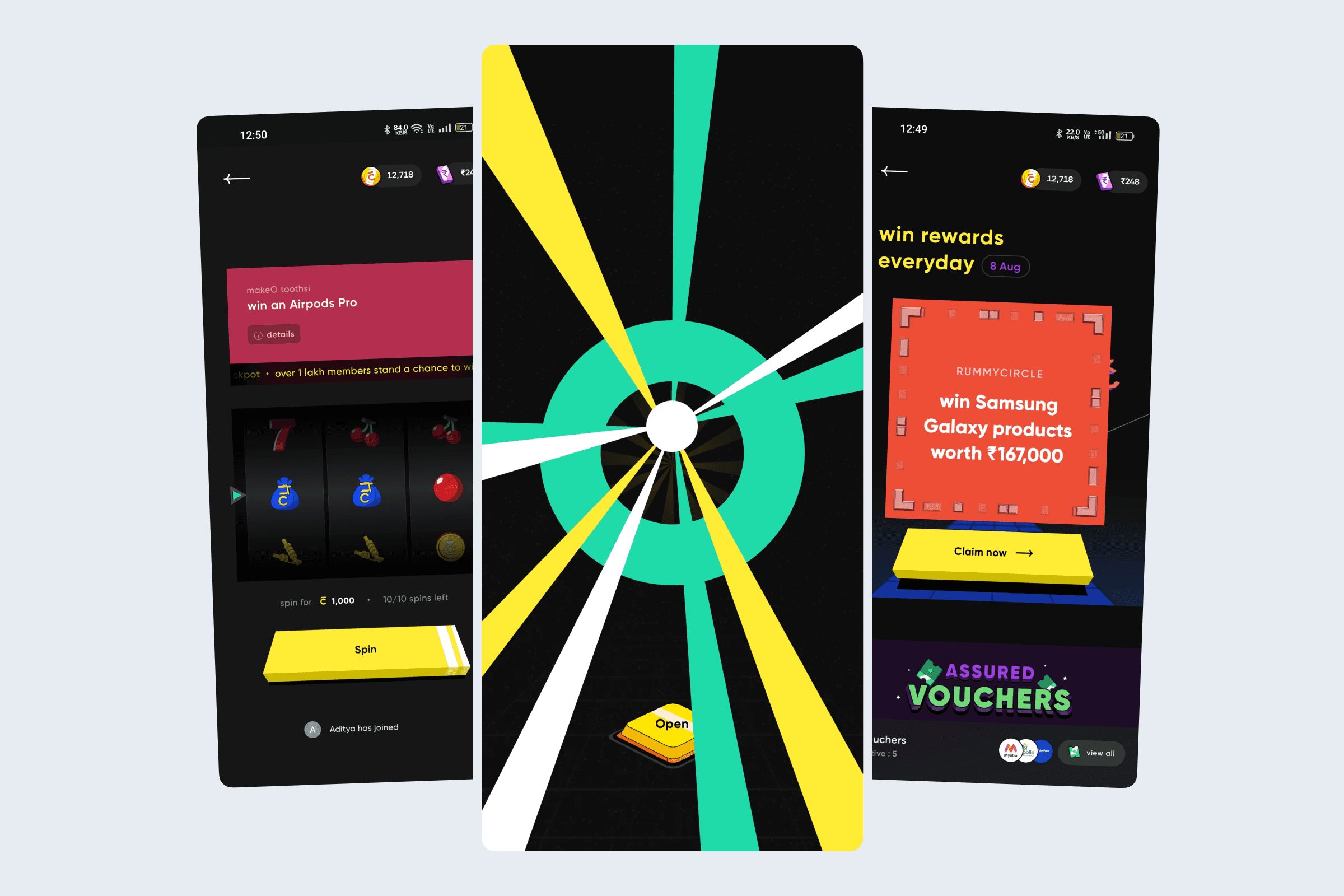

Rewards are central to the app's experience and face a design overkill. It feels like entering into a casino, which is perhaps not something I'd want from an app that helps me manage my money.

You also cannot not notice it since it has multiple entry points scattered throughout the app — two prominent ones on the home screen itself.

Spinning the wheel feels wonderful since the animation is cool and you anticipate a reward. After a couple dozens rounds though, the animation starts to feel frustrating and slow — especially after you realise that the rewards are scanty. And also because it suffers from finite variability, as defined by Nir Eyal in Hooked. But you can't stop since the motivation is monetary. That makes me think that despite high usage metrics, feature perception can still be negative.

Animations build anticipation but they become intolerable since you almost never feel rewarded, rather mostly cheated of your time. In most other games, you can usually tap to speed through the animation which isn't possible on CRED, adding to the frustration.

Suddenly, you always start winning a voucher on the slot machine game, and that too on the first spin itself! Eventually, that stops feeling like winning, but more like it was designed for you to win. You start to doubt that the game is rigged and lose trust. The animations start to look like blinding lights — the kind where you win ₹2 as compensation on a good day.

It is also the #1 reason why I don't even open the CRED store and the travel section to browse for offers.

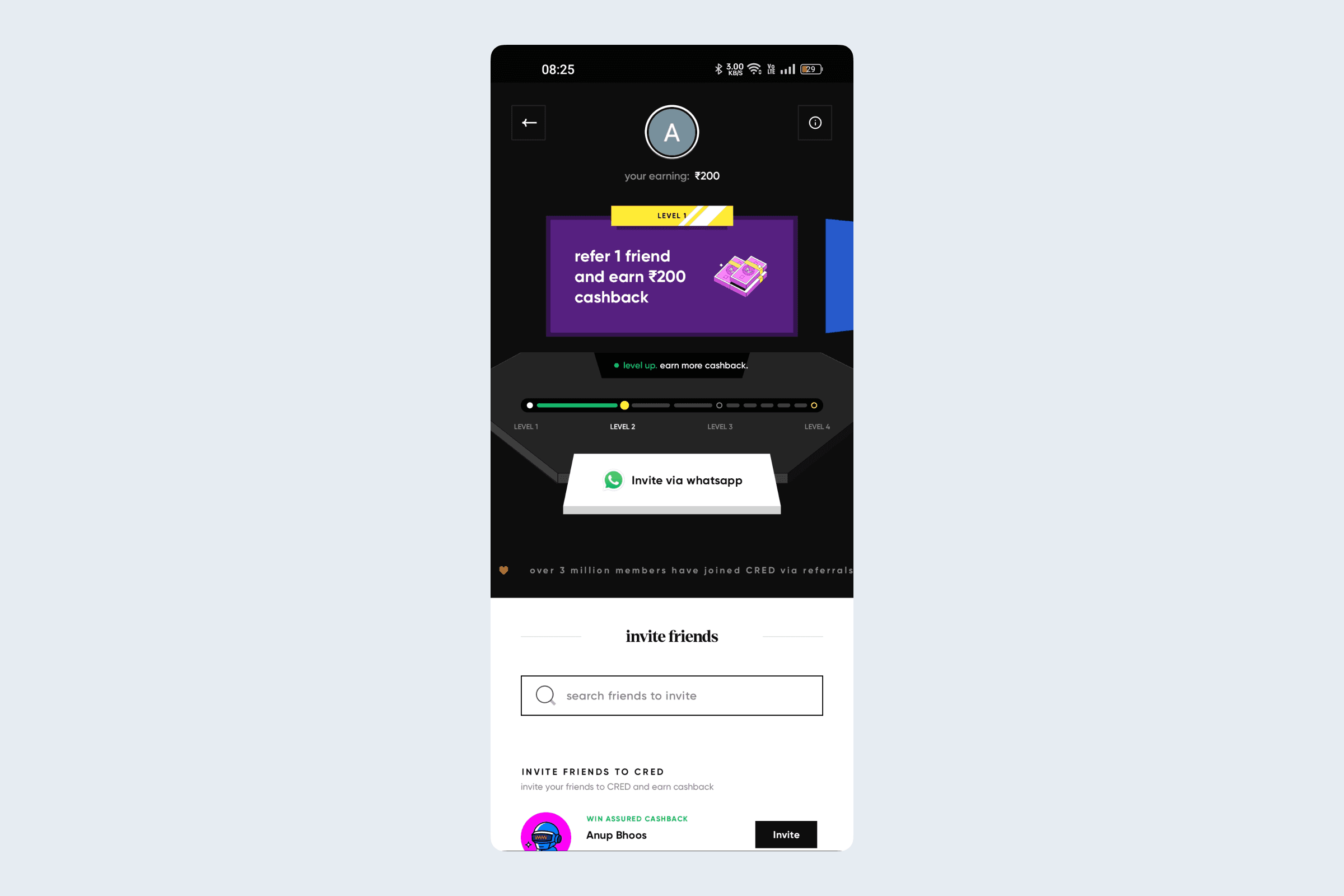

Referral system

On the referral screen, communication of the offer is plain bad. I went from thinking I'd get a ₹1000 cashback to ₹500 to actually getting ₹200. Sigh!

And why are there levels to this? I'd assume the idea is to reward the user increasingly more to perk them up to keep referring CRED to more people.

But instead of designing a complicated game around this (with hard-to-understand rules), why not simply increase the referral amount every time a successful referral is completed. That way the user feels incentivised for their evangelism and the added amount comes around as a positive surprise.

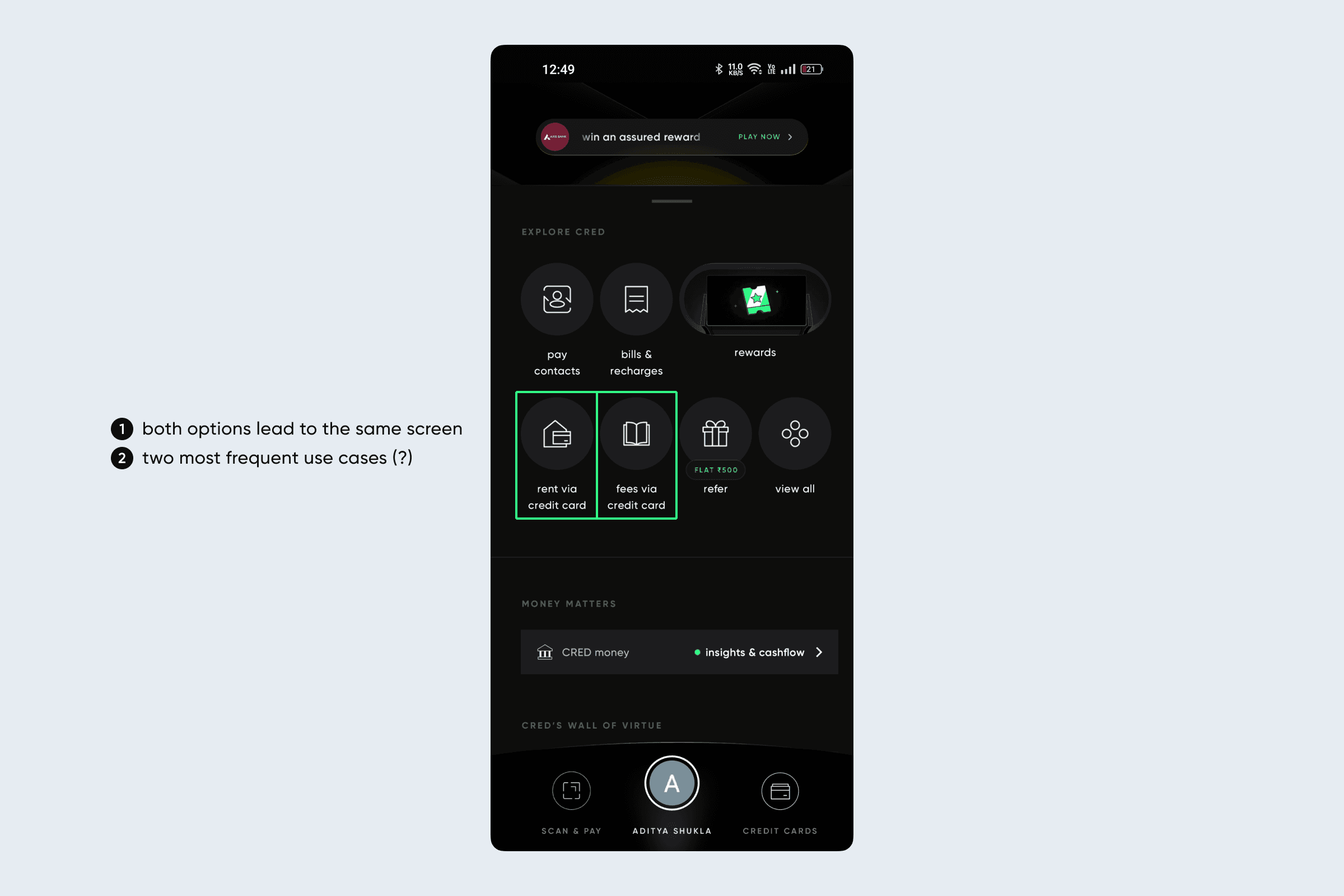

Quick credit

Revenue from loans forms a good chunk of the overall revenue. Consequently, it appears prominently on the home screen TWICE — framed by the most popular use cases. I think it's pretty clever. This feature is also promoted on almost every screen in the app.

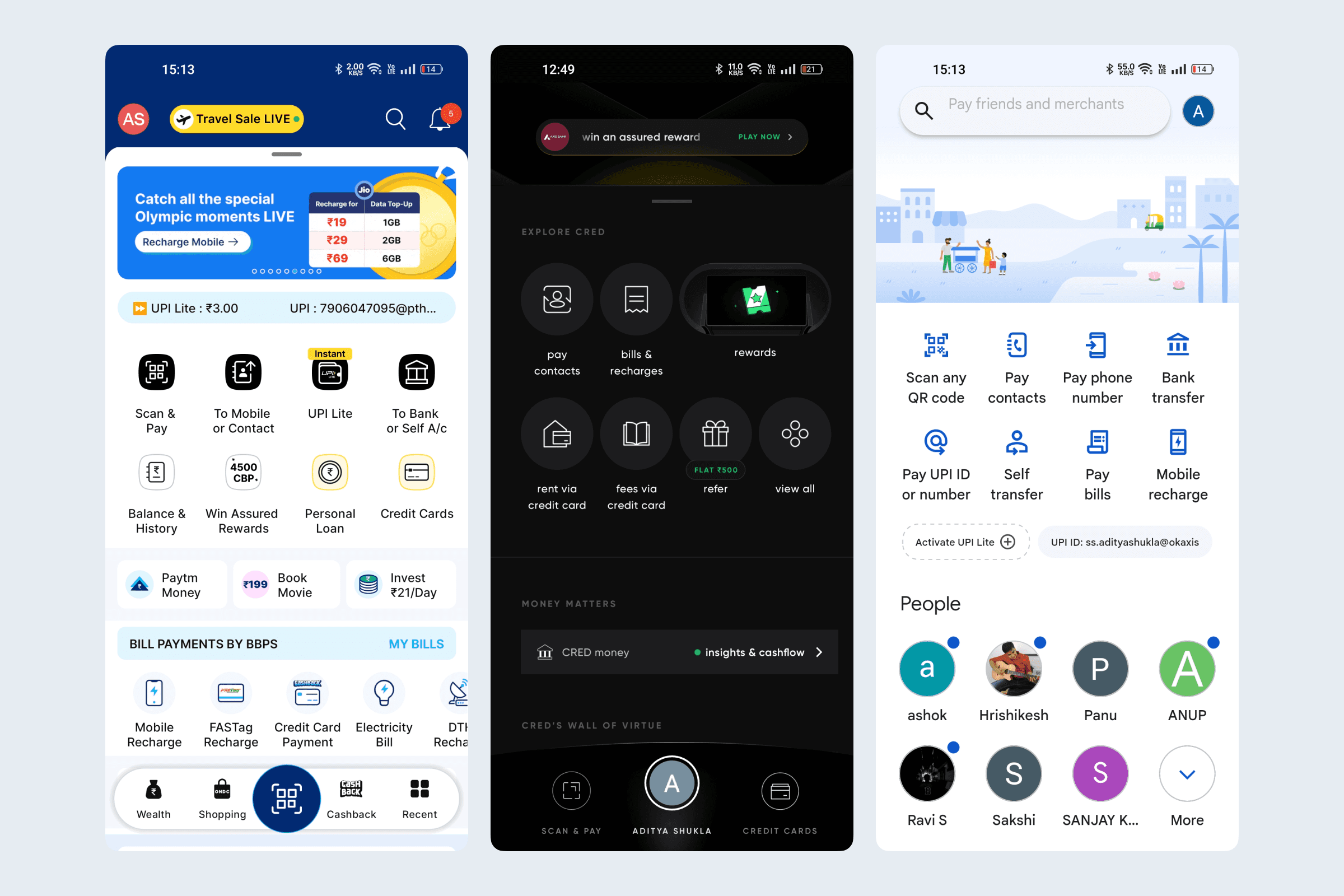

Comparison with other apps

Since CRED has moved away from just being a credit card app, it's interesting to compare the interface with Paytm and Google Pay.

Some observations:

CRED's interface is cleanest of the lot. But I often feel that it's designed like a well-appointed roof deck, in total contrast to Paytm's approach.

CRED has kept the UPI segment away from rest of the app for the most part, which was a later addition anyway. I think it makes sense and also leads to a less confusing interface as compared to say Paytm.

CRED has cleverly highlighted use cases of quick credit instead of calling it "Personal Loan" like Paytm. This makes it more approachable and less daunting.

Finding transaction history is pretty hard in the CRED app. It's hidden beneath 2-3 screens, which is a pain — it's a roof deck accessory. Both Paytm and Google Pay have made it easy to see transaction history and bank balance.

I don't understand the need of repeating the "rewards" section on the home screen itself. It can rather be used to pitch a couple more services. But would that make the interface more cluttered?

CRED Money does allows you to view your bank balance and transactions from the home screen. It's good placement too. But since it picks up vendor name from the AA, the transaction list is pretty useless. It would be better if it can pick and match UPI vendor names against the transactions.

Credit cards screen

Finally the credit cards screen in the app puzzles me every time I open it. I always need a couple of minutes to figure out the information myself. It's easier to recognise information than to recall it. CRED should really use this principle in their designs.

It's hard to figure out the current cycle for each card. For me, it's the most important thing to make sure I have paid all my bills and can relax.

The "Pay now" button lies on the card, which itself is tappable.

The expenses incurred in the current cycle is shown devoid of any charges/fees charged by the bank. That's why there's always a mismatch between what appears on CRED and on the bank app. This causes unnecessary confusion.

Barring this nitpicking, I think the app is quite tastefully designed. Oftentimes, the form is emphasised more than the function. It's designed to feel different from the traditional bank apps—funky, pop and cool. It does too much for my taste but I still use it everyday. That says a lot about the design.